Your cart is currently empty!

NetOne has nearly 2 million customers it is not chasing

Welcome to our weekly roundup, where we bring you interesting insights from different industries condensed into a quick and informative read. Buckle up, because whether you’re a business leader, policy fanatic, or simply curious about the region, this newsletter has something for you. Stay informed, stay engaged, and have a good weekend!

Sign up to our mailing list to get the weekly roundup straight in your inbox

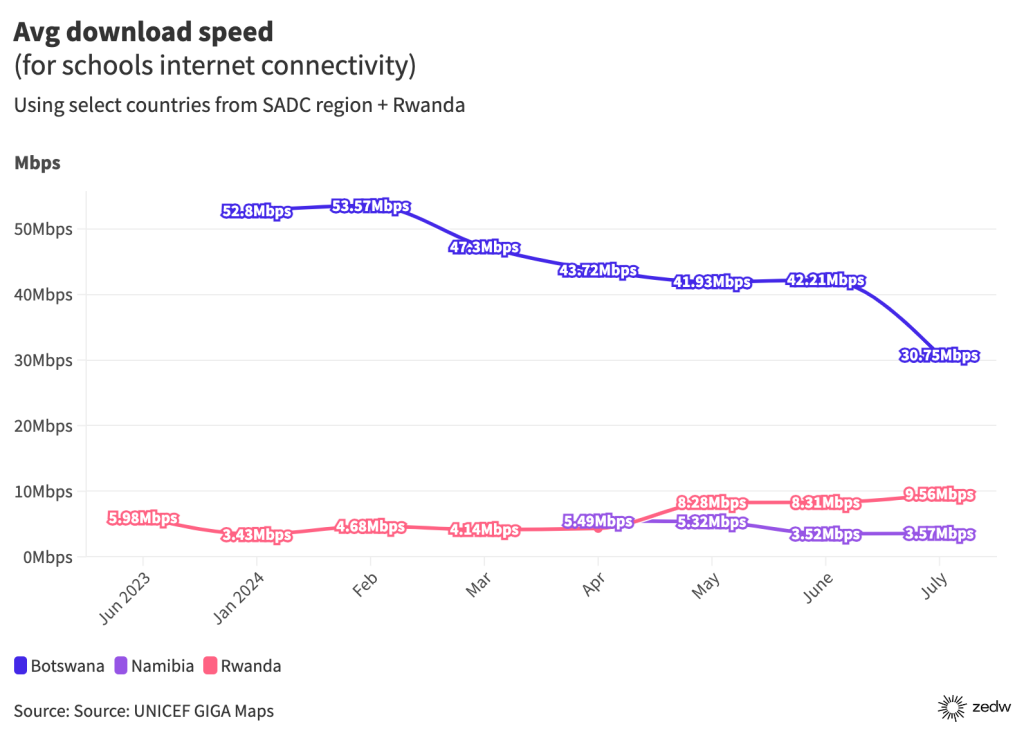

One of the big selling points that has been pitched to governments by citizens in our region hoping that Starlink gets approved has been that schools stand to benefit from the connectivity. All this got us wondering just how true this is and how big the gap is when it comes to internet in schools in the SADC region. We looked at 2 metrics, connectivity and average download speed (courtesy of data provided by UNICEF’s GIGA Maps portal) to try and figure out the lay of the land – the only limitation is that data was only available for 5/16 SADC countries so our sample is relatively small but what can one do?

Whilst Rwanda isn’t in Southern Africa – it is important in this hypothetical because it was one of the earliest Starlink adopters in Africa, with the service being licensed in February 2023. At the time of the services licensing the country’s Ministry of ICT announced that connectivity for schools would be a big priority. It was also revealed that Rwanda had already connected 44.5% of schools in the country back then and a further 500 would be connected via Starlink. The % of schools connected has since risen by 14% to 58.54% in the 17 months since Starlink was licensed in the country. It seems the state is indeed delivering on what they promised.

When we look closer to home the picture is more complex. Botswana seems to be doing relatively well without Starlink (which recently got licensed in the country) with 54% of schools connected. Whilst this number appears high in comparison to the low performers it’s important to note that nearly every other school in the country has no connectivity. Lesotho and Zimbabwe perfectly illustrate why the clamouring for Starlink is so loud and why the potential connectivity benefits for schools is a recurring theme. With 14.1% and 27.8% of schools connected respectively, there is a huge gap and it goes without saying that nearly all primary and secondary students in these countries have no internet access.

Namibia and South Africa have the highest connectivity rate among the countries included in the data sample at 67.3% and 63.5% respectively, but unfortunately the data for these two is a bit muddy for our liking. UNICEF’s GIGA data on these 2 countries have done the good work of tracking which schools are connected but they haven’t highlighted which schools aren’t connected making it hard to determine how large the connectivity gap in these countries is.

The secondary metric which we wanted to track was speed, because it’s not as important as having the access to begin with but also because the sample data is even more limited than the connectivity data we just looked at. Still we will take a look at the data available (but no hot takes this time around:

Remember this is a SMALL SAMPLE SIZE and I would suggest we don’t know enough to make assumptions about what could be impacting speeds. Regardless, I do think those arguing for Starlink licensing will shout, “the country distributing Starlink units to schools has doubled internet speeds whilst the countries which haven’t bought in have experienced a decline.” It’s a bit of a reductionist argument, in my opinion, given that we don’t know the degree to which Starlink is the cause behind Rwanda’s improved speeds.

This section was longer than I envisioned so let’s move on to the next order of business…

Sign up to our mailing list to get the weekly roundup straight in your inbox

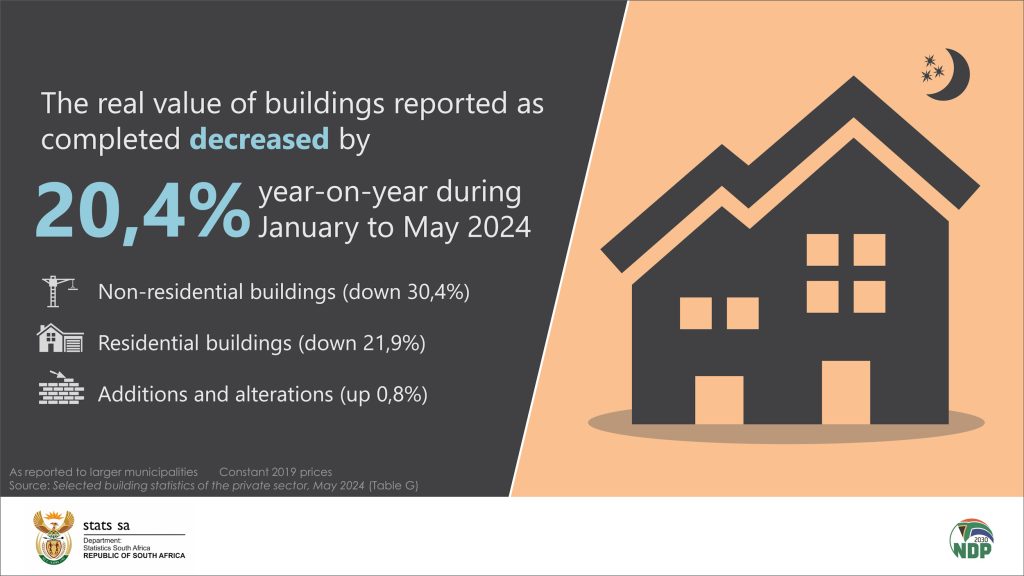

Recent statistics from StatsSA point to a shift in South Africa’s construction industry. The overall picture is that fewer building plans were approved for the first half of this year compared to last. Building plans submitted for future construction projects and renovations seem to be more modest in value compared to the same period for 2023:

Interestingly, the similarly negative outcome extends to projects that have already been built during the first half of the year:

In simpler terms, this just means that fewer buildings were completed between January and May 2024 compared to the same period in 2023. All of this begs the question, what’s affecting South Africa’s construction industry? Back in May, Business Tech detailed some of the issues affecting the construction industry and boy is it a complex situation.

These are just a few of the many reasons but to say the impact all of this is having on South Africa’s construction industry is significant would be an understatement.

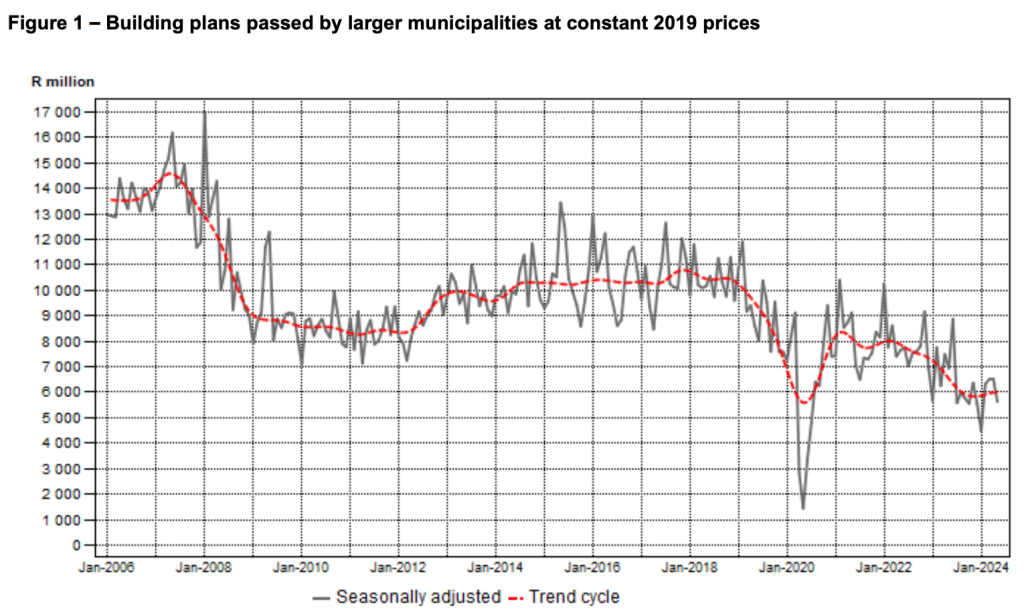

The value of building plans passed by larger municipalities had fallen from a peak of around R17bn (in 2008) to just below R6bn in January 2024. HECTIC.

Sign up to our mailing list to get the weekly roundup straight in your inbox

Zambia Information and Communications Technology Authority (ZICTA) issued a statement earlier in the week addressing (or attempting to) the impact load shedding is having on telecoms service delivery. The statement reads like a non-statement from an entity that understands both consumers’ frustrations and service providers limitations.

“As part of our mandate to ensure that consumers experience high quality electronic communication services, we have continued to monitor the impact of electricity load management on the quality of voice and data services experienced by consumers. We have equally noted the persistent challenges reported by members of the public.”

ZICTA

Given that the country has been experiencing 14 hour power cuts, it comes as no surprise that service delivery is being affected. Global System for Mobile Association of Zambia (GSMAZ), a telecoms lobby group owned by MTN Zambia, Airtel Zambia and Zamtel issued their own statement a week ago following customers complaints regarding poor service delivery. The lobby group explained that load shedding is causing “a huge cost variance not only for the fuel and generator maintenance but also for the associated fuel delivery logistics.”

Ultimately this sounds to me like both the regulator and service providers suggesting that what’s happening is largely out of their control. If you’re a consumer relying on these services in Zambia, our thoughts and prayers are with you. Things probably aren’t changing anytime soon…

Sign up to our mailing list to get the weekly roundup straight in your inbox

Featured

Gain access to premium content and stay up to date with the latest insights

Unlock potential and investment opportunities with precise market insights from .zedw newsletter.