Your cart is currently empty!

NetOne has nearly 2 million customers it is not chasing

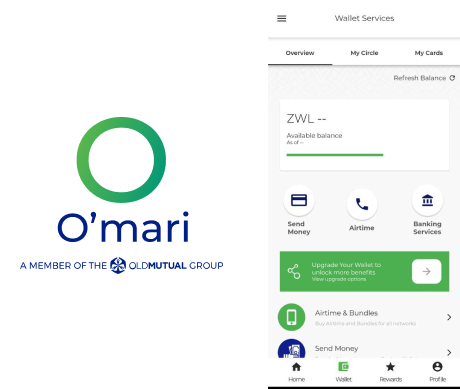

Not every founder has the luxury of an almost century-old business with a diversified portfolio as a launch pad. Moreover, a litany of industry-agnostic partnerships and shareholdings ensuring whatever is dreamed up has more than a fighting chance. This is what O’Mari essentially is and we know at this junction, […]

Featured

Gain access to premium content and stay up to date with the latest insights

Unlock potential and investment opportunities with precise market insights from .zedw newsletter.