Your cart is currently empty!

NetOne has nearly 2 million customers it is not chasing

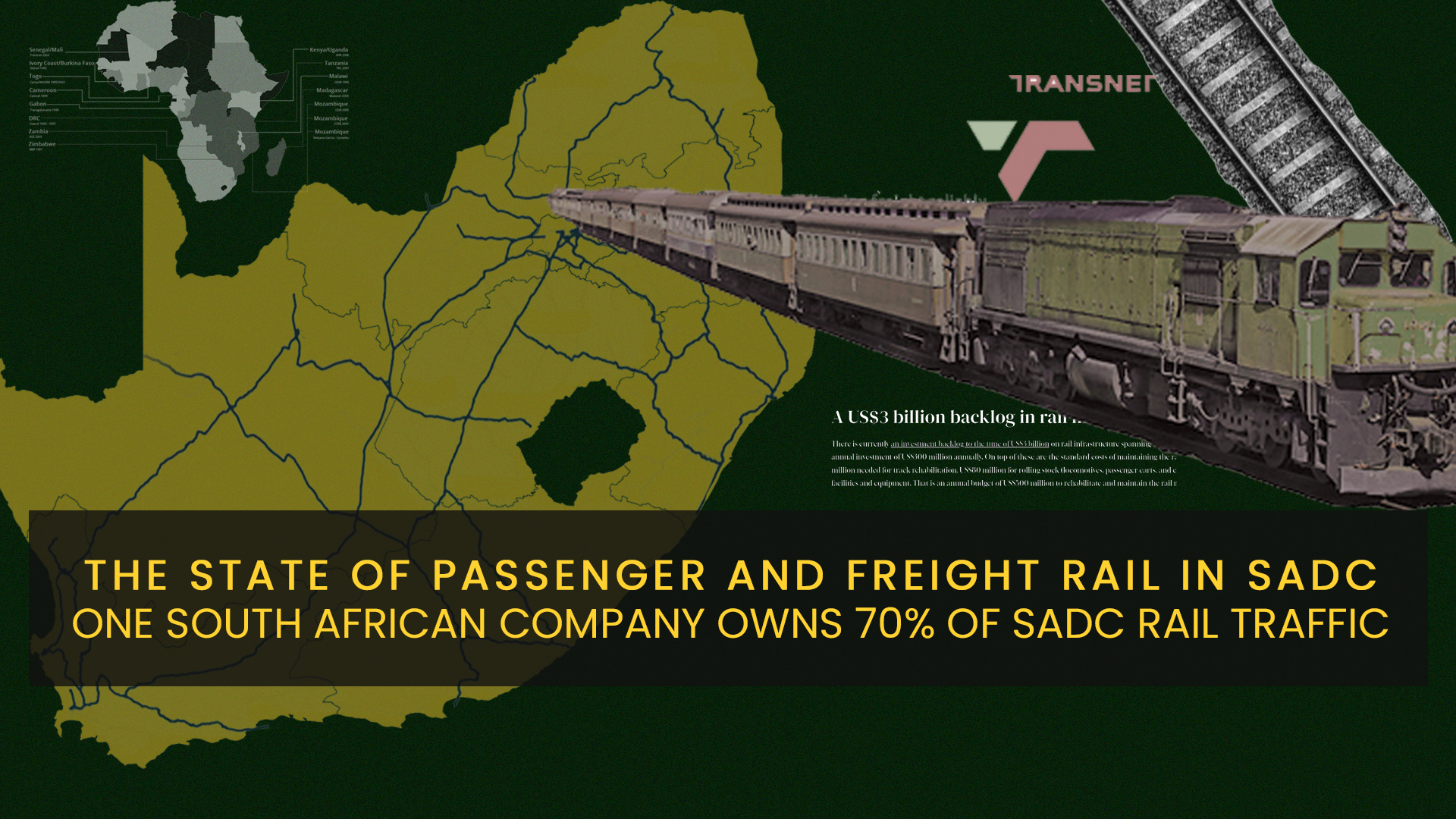

The state of rail for logistics and passenger transport in the Southern African Development Community (SADC) is a far cry from where it could be. Just as a quick refresher, there are 4 main modes of freight of goods and passengers road, rail, maritime, and air. Of all those, rail […]

Featured

Gain access to premium content and stay up to date with the latest insights

Unlock potential and investment opportunities with precise market insights from .zedw newsletter.