Your cart is currently empty!

NetOne has nearly 2 million customers it is not chasing

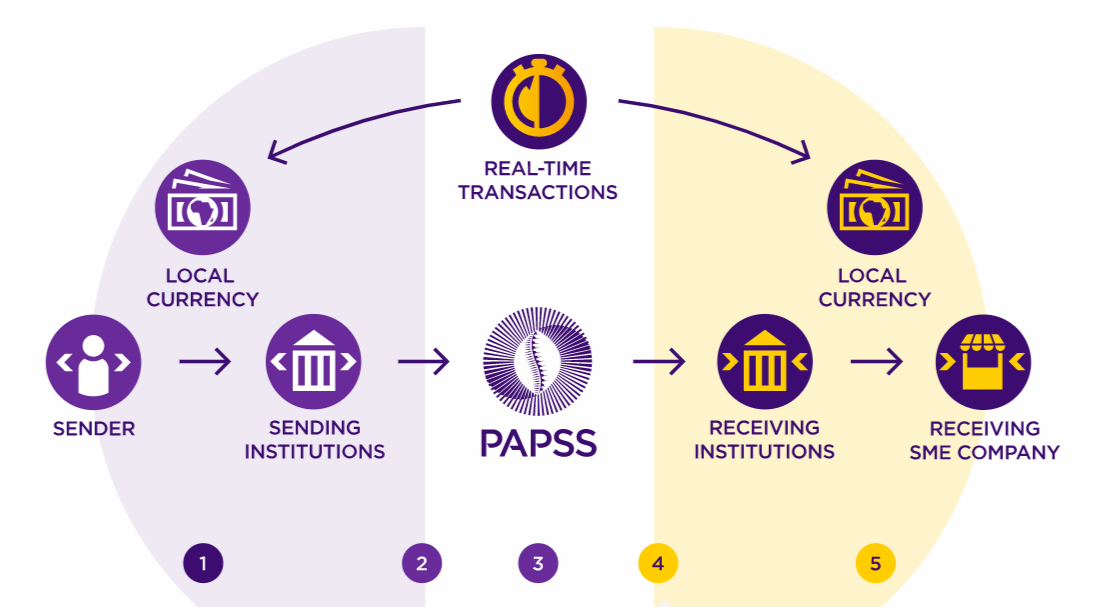

The Pan African Payments and Settlement System (PAPSS) is right around the corner even though there seems to be a lull in anticipating an innovation that looks to revolutionise African payments. Gone will be the dependency on foreign services that are not precisely attuned to the kaleidoscope of African operating […]

Featured

Gain access to premium content and stay up to date with the latest insights

Unlock potential and investment opportunities with precise market insights from .zedw newsletter.